BW Energy's challenging path to dividends

Assessing BW Energy's strategy towards shareholders' returns

A great investor, Calvin Froedge, has announced the publication of an analysis of BW Energy. It seems that the company is getting more and more attention, and I decided to update and expand some aspects I covered in my previous write-up about BW Energy.

He has also speculated that BWE could offer an interesting dividend yield from today's levels at 26.x NOK per share. However, I think the company has a lot in its plate right now, and I see unlikely that a dividend will be paid soon. I'll go through the main assets the company owns and what the picture could be in the next few years. The company has many assets and growth opportunities for the coming years, but I doubt there would be enough left for shareholders' retribution unless they sell some assets. The company has already provided an overall picture for the right moment when dividends would begin, but given all the open fronts, I believe dividends are unlikely before 2026, as earliest.

Let’s take a dive at BWE’s main assets in Gabon, Brazil and Namibia to assess the current status of each, and what alternatives there are in the coming years to materialize the potential value.

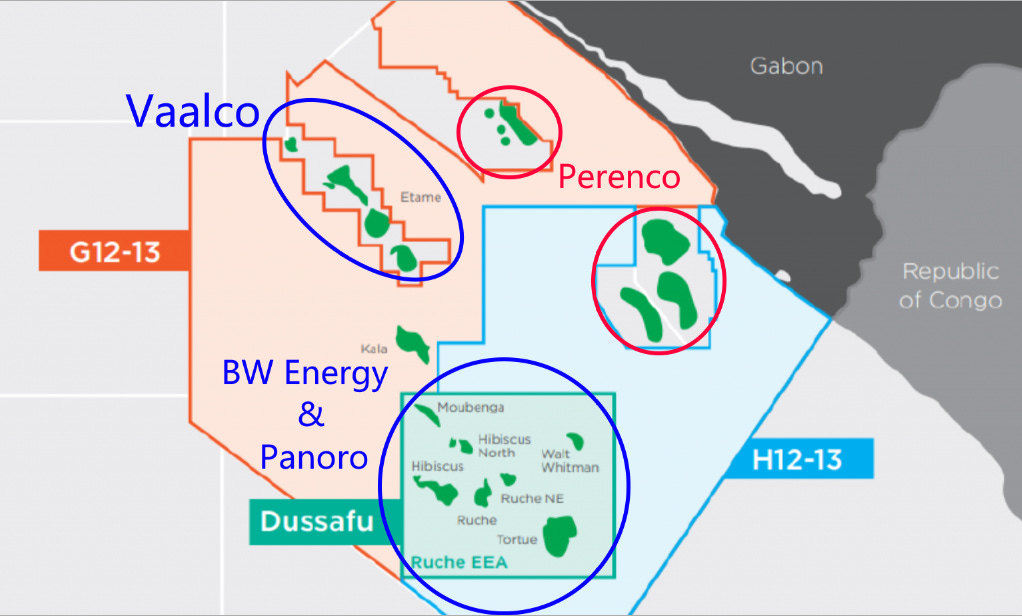

Gabon - Dussafu and G & H blocks

Recently, BW Energy announced the successful start of production from the second well in the Hibiscus/Ruche Phase 1 development offshore Gabon. The DHIBM-4H well is currently producing around 6,000 barrels per day, meeting expectations. The well was drilled horizontally to a depth of 4,800 meters into the Gamba sandstone reservoirs of the Hibiscus field. The Dussafu field is operated by the BW Adolo FPSO and the BW MaBoMo (a repurposed jackup rig).

Additionally, the commissioning and testing of the second gas lift compressor on the BW Adolo FPSO are ongoing, with expectations of adding another 3,000 barrels per day to production once fully operational.

The drilling campaign includes four Hibiscus Gamba and two Ruche Gamba wells, with a projected total oil production of 30,000 barrels per day when all wells are completed by early 2024. The oil is transported through a pipeline to the BW Adolo FPSO for processing, storage, and export. All funding is covered by the $300M RBL facility signed with banks.

In 2021, BW Energy was awarded a 37.5% WI in two exploration licenses, G12-13 and H12-13, together with Panoro Energy (WI 25% and partner in Dussafu) and Vaalco Energy (WI 37.5%). These licenses will benefit from the knowledge of the most active producers in the area and their geologists count with access to exclusive data on the different reservoirs in the area. The partners are negotiating a PSC with the Gabonese government and committed to reprocess the existing seismic data, complete a 3D seismic campaign, and drill one well in each block. This gives the company additional upside beyond 2026, in case the exploration campaign is successful. Currently, the commitment of the partners for the G and H blocks seems light, and we may see a couple of drills in the next five years. I beilieve it is unlikely that the FID for any of these 2 blocks begin before 2026, in the most optimistic scenario.

The production from Dussafu alone will be above 30,000 boepd (22,000 boepd net to BWE) in the next years, which is substantial. This high production from Dussafu and low development commitments for the G and H blocks will make Gabon THE cash-cow for BWE in the coming years, as most of the profit generated at Gabon will be available for the company to invest in other assets or return to the shareholders.

Brazil - Maromba & Golfinho

The two assets owned by BWE are dramatically distint: Golfinho is a mature asset operating in deep waters (currently closed due to required safety-related upgrades in the FPSO), and Maromba is a greenfield in shallow waters.

The Golfinho transaction is nearing completion. I wouldn't be surprised if the announcement was made in the coming weeks. The acquisition was delayed by the decision of the Brazilian government to halt Petrobras' divestments, but it has been resumed, and there aren't any indications that could lead one to believe it won't be closed.

BWE has acquired a 100% operated working interest in the Golfinho and Camarupim clusters, as well as a 65% interest in the BM-ES-23 block in Brazil. The company is also acquiring Saipem's FPSO Cidade de Vitoria (with a cost of $73 million: $25M at closing, $13M at FPSO takeover and $35M in 18 monthly instalments following the takeover), which operates the Golfinho field. The acquisition involved an initial cash payment of $15 million, with up to $60 million in contingent payments linked to oil prices, well operations, and further development. BWE will assume the abandonment liabilities for the FPSO, subsea infrastructure, and 13 wells, of which Petrobras will share the cost of four wells. The estimated proven recoverable resources in these assets are around 38 million boe, with 19 million boe already developed and producing. The company has identified additional gas accumulations of approximately 0.7 trillion cubic feet (Tcf) for potential future development. The Golfinho Cluster is located at a water depth between 1,300 and 2,200 meters in the Espírito Santo Basin, and the Camarupim Cluster is non-producing and is in water depths between 100 and 1,050 meters.

One of the conditions is that Petrobras must restart the FPSO after implementing the upgrades required by ANP. The status of the FPSO raised serious concerns among the ANP officials due to safety risks. One of Brazil’s unions tried to block the transaction citing the case of the FPSO Cidade de São Mateus operating the Camarupim and Camarupim Norte fields owned by BW Offshore (BWO), which exploted in 2015 and caused several deceased. The Camarupim and Camarupim Norte fields have been closed since the incident in February 2015. Coincidentally, BWE is a spin-off from BWO, so, technically, BWE was the operator of these fields that it has now acquired. This seems to be an overlooked aspect by most investors, BWE’s team knows perfectly all the particuliarities and challenges of these fields, and they will operate them thanks to receiving the offshore operator license by ANP. Moreover, the solution that Petrobras proposed to the ANP for the resumption of the production from the Camarupim and Camarupim Norte fields included the use of the FPSO Cidade de Vitoria that BWE is now acquiring:

Petrobras also analyzed other technical alternatives, such as a jacket, the interconnection to FPSO Cidade de Vitória, in operation in the neighboring field of Golfinho, and the installation of a smaller FPSO.

Once all the conditions for the closing of the transaction are met, BWE expects to add 9,000 bopd to its production base after closing the transaction. The development cost of the Camarupim and Camarupim Norte gas fields doesn't seem significant compared to Maromba. The gas fields were in operation so the wells and subsea infrastructure is already there, it appears that they only require a new FPSO or FSO capable of receiving and processing the gas from the fields. The remaining prospects included in the Golfinho and BM-ES-23 blocks don't seem to be relevant for the next three years, at least.

Hence, I believe the Golfinho transaction is simply brilliant. They have acquired a field that will be producing from day one at a very low price. The primary liability they will receive is the FPSO, which they will operate without a contractor, further reducing the breakeven point. They could potentially sell it to BWO if they need liquidity. The upside potential from the Camarupim fields is substantial, thanks to their knowledge gained by BWE’s team during their time as operators of the FPSO connected to the wells. As a result, the Golfinho acquisition will generate positive cash flow from its closure and has the potential to add value for the next few decades.

Regarding Maromba, one important aspect to consider is that it is located at water depths of 160 meters and very close to other fields in the Campos Basin, which will allow it to benefit from synergies with adjacent operators. Petrobras also sold the Papa Terra field to 3R Offshore in 2021, and Equinor is operating the Peregrino field after completing significant upgrades to the FPSO, with plans to extend production until 2040. The area has been highly productive and offers further development opportunities that could potentially sustain production in the Campos Basin until 2050.

BWE acquired the FPSO Polvo from BWO for $50 million in Q2 2022 to be used in the Maromba field. This FPSO was previously used in the Polvo field, which is also in the Campos Basin and produced similar oil. In Q1 2023, BWE reached an agreement with BWO to delay the payments related to the acquisition of the FPSO Polvo, with $30 million scheduled for Q4 2023 and $20 million for Q2 2024. This was expected as BWE had anticipated closing the Golfinho transaction in Q1 2023 and had been investing heavily in the Hibiscus/Ruche Phase 1 development and data acquisition in Namibia, leading to the need to postpone the payments. As a result, nothing has been done with the FPSO Polvo, and the vessel has remained in Dubai, where it has been moored since the contract with PetroRio expired in 2021.

It is important to note that the final investment decision (FID) for Maromba has not been made yet. The company has to secure the financing to complete the acquisition and upgrades of the topside and hull of the FPSO Polvo and the various contracts for the wells and subsea equipment need to be signed. In my opinion, the delay has been caused by temporary financial difficulties resulting from the delay in closing the Golfinho transaction and the high investment required for the Hibiscus/Ruche development. Therefore, as production in Dussafu continues to increase and Golfinho is finally transferred to BWE, I think the FID could be announced as early as Q4 2023, being Q2 2024 more realistic. However, the situation has affected the timeline, and first oil from Maromba has now been postponed to H2 2026. Consequently, I don't believe Brazil will contribute significantly to BWE's cash flow in the 2024-2025 period, as most of the cash flow from Golfinho will be directed toward completing the necessary works at Maromba.

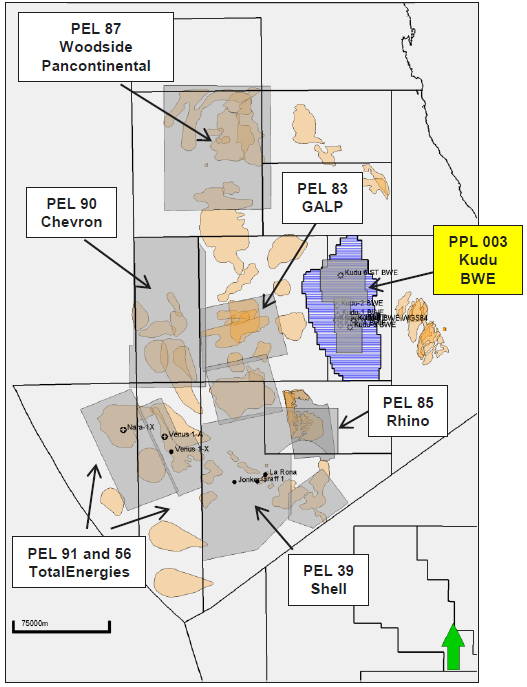

Namibia - Kudu gas field

The company completed the 3D seismic, gravity, and magnetic data acquisition campaign with 5,000 km of high-quality data. This campaign was planned after the results obtained by Shell and TotalEnergies in the Orange Basin, which are deeper (Venus-1 at ~6,300 meters) than Kudu (~4,500 meters). Currently, the company is trying to assess whether there are other potential discoveries that were overlooked in the existing data obtained from seismic campaigns (from the 90s and 00s) and exploration wells.

The initial analysis of the data is expected to be completed by the end of July, with further detailed analysis to be completed in Q3 2023. The final report on this data cquisition campaign is planned for May 2024. Hence, the plans for Kudu could be adapted to the findings of this analysis, and the data can be shared with other license holders in the area. Other companies in the area like Sintana Energy (partner in Galp’s PEL 83) have recognized the relevance of the data acquired by BWE for their own exploration campaigns. Woodside will finance a 3D seismic campaign in the PEL 87 license and Chevron awarded PGS with a contract to run a 3D seismic campaign in the PEL 90 license. Despite all these licenses being independent from each other, the collected data will be critical to understand the petroleum system in the whole area and define the migration of oil and gas from the rock source. A better understanding of the complex geological processes, including rock types, temperature, and pressure, will be key to identifying areas with the potential for oil and gas deposits. It can also lead to a better identification of the presence of a good-quality reservoir with a seal combined with traps where the hydrocarbons accumulate and can be exploited. It is not known whether the different license holders will share data or if the companies acquiring them can resell them (for example, PGS offers a data library with raw 2D/3D seismic data from many areas of the world), but management commented in the Q1'23 CC that they'll put forth a strategy in the future.

BWE already acquired a semisubmersible drilling rig as a floating production unit (FPU) in 2021, which will be repurposed for Kudu. It also has to complete the design of the gas-to-power solution to export electricity to Namibia. It is important to stress that FID hasn't been reached yet. Despite many contracts being completed so far, the Kudu field is still in the Front End Engineering Development (FEED) stage. Once FEED is completed, BWE will begin farm-in discussions for the FID and development stages. The total development costs are expected to be high, for example, requiring a 190km underwater gas pipeline, well above $1.2 billion. Hence, I think the development of the Kudu field may be affected by the outcome of the analysis of the data acquisition campaign, particularly if other prospects are identified, delaying first gas (or oil) beyond 2026. Additionally, BWE cannot standalone finance the development of the Kudu field without the farm-in of a major or supermajor; besides, the existing partner, Namcor (WI 5%), is carried.

It is important to remember that the Kudu field was discovered in 1974 by Chevron, and several attempts to develop it have been made, such as Tullow Oil. For years, oil companies have tried to construct a commercially viable operation out of the Kudu gas field. A key problem is that the field's contingent resources of 1.4 trillion cubic feet of gas are relatively modest, and the geology presents challenges, including a depth of 4,500 feet. Eight wells have delineated the Kudu gas reservoirs, and yet it remains undeveloped. Hence, there may be a chance that BWE also doesn't complete the development, particularly if the results of the data acquisition campaign are not supportive. Additionally, there could be additional upside if Kudu were developed, and its infrastructure were used to transport gas from the Graff or Venus fields.

I don't think BWE will significantly advance the FEED for Kudu until the second analysis of data is available in late Q3 2023, at the earliest. Indeed, the company may put the progress on hold until the final results are completed in May 2024. Moreover, finding a farm-out partner will be a requirement to secure the financial resources to convert Kudu into a productive asset. In my opinion, Namibia will not be completed before 2026, being optimistic, and I wouldn't rule out further delays to 2027 or 2028 if another relevant prospect is identified in the recent campaign.

Conclusion

Despite the companies of the BW Group being known for their dividend policies, I cannot see how BWE will manage to complete all ongoing developments while implementing a dividend policy before 2026. I see the share price accompanying the progress in the different plays, particularly at Gabon and Brazil, but it could also be a bumpy road.

Gabon and Golfinho will play a crucial role in providing the resources to secure BWE's financial position in the coming years. Maromba appears to be a low-risk, high-reward opportunity due to BWE's experience in the Camarupim fields. Assuming operatorship of the Brazilian fields is reducing the breakeven point.

However, the development of the Kudu field is quite expensive, and finding a farm-out partner will be critical to its completion. Additionally, there is uncertainty regarding the outcomes of the data acquisition campaign, which could have both positive and negative impacts. It is important to consider that if promising prospects are identified during the analysis of the data, an exploration campaign will be quite costly and delay Kudu’s development even more, but will increase the interest among potential farm-out partners.

In the second half of 2023 and 2024, I expect that we will witness high production from Dussafu due to the completion of Hibiscus/Ruche Phase 1 and the first contributions from Golfinho, reaching a net production of 30,000 boepd. It seems challenging to imagine a scenario where BWE does not generate a significative amount of cash in 2024, considering the main investments are the completion of Hibiscus/Ruche Phase 1 and the acquisition and upgrade of the FPSO Polvo. Additionally, acquiring (upgrading?) or leasing an FPSO or FSO to restart the Camarupim cluster between 2024 and 2025 is a possibility, but the impact should not be relevant. However, the final investment decisions for Maromba and Kudu remain pending, and, if everything goes according to plan, a significant amount of cash will be required in 2025-2026 for the development of both.

In summary, I believe BWE has significant potential, but it is a medium-term investment. While the company can maintain production around 30,000 boepd during the 2024-2025 period, it will be working towards a remarkable increase in production to 60,000-80,000 boepd by H2 2026 or H1 2027. I think that’s the moment when the company will begin the payment of dividends, but I don’t discard that BWE could begin a token dividend after Maromba’s FID.

These are just my hypotheses, and I look forward to reading Calvin's article, as I'm sure he will present well-reasoned arguments to support his vision.

Disclaimer: this document only represents the opinion of its author; its content cannot be considered investment advice and it has been prepared only for informative purposes. Please, make your own due diligence and analysis.