Orcadian Energy: a new life

An underdog company with a promising oilfield in the UK

This post was sent to our subscribers after the announcement of the HoA signed by Orcadian Energy with a North Sea operator. We organised a meeting with the company to present it and have a Q&A session. Remember to subscribe to join future opportunities like this.

Orcadian Energy (LON:ORCA) is a North Sea focused oil and gas development company with a current market cap of £14.3M (£7.2M at the time of the email). The Company’s key asset is the 100% interest in the Pilot oilfield, with proven and probable reserves of 78.8 million barrels (audited by Sproule BV). The Company also owns other discoveries like Elke, Narwhal and Blakeney.

The company announced on the 18th of September a Heads of Agreement ("HoA") with a potential farm-out partner for the development of the Pilot oilfield in what seems good terms for the company.

The Pilot field

The main asset is the fully appraised Pilot field that contains sweet, heavy oil in the Central North Sea. The company also owns other adjacent discoveries, but they are less mature. The oil found at Pilot is viscous with API gravities ranging from 12° to 17°, lower than typical light oils in the North Sea. This oil is a rarety in the area and can supply refineries in UK that usually have to source it from more distant fields.

The Pilot field is divided into Main (230 OIIP MMbbls) and South (33 OIIP MMbbls) structures, where 7 wells in total have been drilled. According to the CPR, the reserves are:

1P: 58.5 MMbbl

2P: 78.8 MMbbl

3P: 110.5 MMbbl

In January, the company, with support from Axis, interpreted newly reprocessed seismic data from TGS, which resulted in an uplift to the developed area oil-in-place. TRACS constructed a range of geological realizations and ORCA’s team ran multiple dynamic reservoir simulations to establish a new range of technically recoverable resources. As a result, the company reported an upgrade of the recoverable resources to 65.3 MMbbl for a P90 case, 97 MMbbl for a P50 case and 131 MMbl for a P10 case. These amounts are not included in a CPR.

The NSTA has already approved the initial design concept and has also extended the license to November 2023. The Field Development Plan (FDP) hasn’t been completed and it is part of the conditions included in the farm-out agreement. Part of the work done has prioritised the reduction of scope 1 and 2 emissions, including a study to “evaluate a new concept for the electrification of key producing oil and gas fields”. The company produced the "Orcadian's Microgrid Concept" for the electrification of offshore infrastructures. The design contains floating wind turbines backed by highly responsive gas-powered generators, acting as battery power, which will use the associated gas produced in the oil extraction. As a result, the need for an energy (gas or electricity) supply from shore will be eliminated, which lowers the development expenditure and operating costs. Additionally, Pilot would max out the allowance to 109% of CAPEX under the current Energy Profit Levy, covering part of the CAPEX. This could be of the interest of many major companies that prioritise low-emission greenfields.

Last November, ORCA reported a binding Memorandum of Understanding (MoU) with SLB for the exclusive provision of drilling and completion services and equipment for the Pilot project. The status of this MoU is unknown.

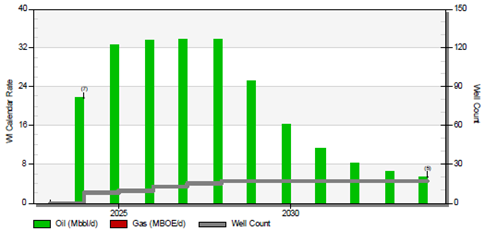

Initial estimations of the development costs are not clear and they range between $720 million (www.offshore-technology.com) and $1,140 million (Sproule’s CPR), but they correspond to the previous design, which will change during the FDP. Despite the high CAPEX estimated by Sproule (which included the acquisition of a FPSO), the NPV10 of Pilot was $159 million of Proved reserves and $654 million of Proved + Probable reserves. The production curve for the 2P case looked like this.

The last concept presented yesterday by ORCA includes a 3-phase development, with 5, 5 and 22 wells drilled, respectively. Phase 1 will require a FPSO and Phase 3 a platform. The low number of wells doesn’t match with the previous information disclosed, which implies a reduction in the recovery factor, but it correspond to a different configuration of the wells and drilling techniques:

The different colours in the figure above represent the injection and producing wells corresponding to the use of polymer flooding. The company estimates that the use of an enhanced oil recovery (EOR) technique like polymer flooding from first oil will increase the recovery factor above the UK North Sea average of 43%. This technique is not common in the UK, with Ithaca‘s Captain field being the best example.

Other assets

Among other licences, other relevant assets present in licence P2482 (which are included as conditional in the HoA recently signed) include:

Elke: Best estimate OIIP 130 MMbbsl, 1 successful well, excellent reservoir quality.

Narwhal: P50 OIIP 26 MMbbls, 1 successful well and 1 dry well, excellent reservoir quality.

The company signed 2 farm-out agreements with Rapid Oil (announced on 11 January 2023) and Carrick Resources (announced on 3 August 2022) for prospects in the P2320 licence. Unfortunately, the NSTA didn’t grant an extension of the licence and both agreements couldn’t proceed.

The company has continued to improve the knowledge over its licenses, acquiring seismic data from TGS (in exchange of a 1% royalty) for the Narwhal-Elke area.

Potential farm-out deal

The company announced the signing of a non-binding HoA with a North Sea operator. The name of the potential partner is yet unknown, but the conditions seem favourable for ORCA under the present situation. Hence, it’s a provisional agreement subject to several conditions, negotiations and due diligence. The main conditions are:

The partner will acquire 81.25% and the operatorship.

ORCA will retain an 18.75% carried interest until first oil (which includes only the phase 1 of the development)

Both partners will prepare a Field Development Plan ("FDP") for NSTA’s approval, using polymer flooding from first oil.

Both partners have requested that NSTA extend the second term of licence P2244, currently until November 2023 and will request an out-of-round award of licence P2320.

ORCA will receive US$100,000 from the partner on completion of each item: extension of the P2244 licence, and a licence award over former P2320.

On approval of the FDP, ORCA will receive US$3 million from the operator.

Financial situation

ORCA is pre-revenue and all its funds come from placings and some minor grants. The company disclosed on the 18th of September a cash balance of £92,000 with a monthly burn rate below £20,000. As a result, it announced a placement in October to raise £350,000. Thus, it has completed several placings and conversion since IPO:

June 2021: placing of £3 million at 40p/share.

July 2021: conversion of Loan Notes into 3,928,572 ordinary shares at a price of 28p each with a value of £1.1 million.

June 2022: placing of £1 million at 35p/share.

February 2023: placing of £0.5 million at 10p/share.

October 2023: placing of £0.35 million at 12p/share.

It is obvious that the company currently lacks the necessary funds to complete the development of Pilot without the support of a partner. Hence, an additional placing should be expected even if the HoA progresses into a farm-out agreement and the approval of the FDP is delayed.

ORCA isn’t debt-free and owes £1 million to Shell’s STASCO, amount that has progressively grown due to the interest. The maturity date has been extended several times, being 13 March 2024 the current repayment date.

Currently, there are 75.4 million shares outstanding with 40,000 warrants with an exercise price of 40p and an expected life of ca. 2 years.

Management and table cap

The executive team is composed of experienced personnel in the North Sea:

Stephen Brown, founder and CEO, a petroleum engineer and held positions in BP, Halliburton, Challenge Energy, Petrofac and Setanta Energy. Steven is the largest shareholder of the company with ca. 40% of shares.

Alan Hume, CFO, has held positions in Halliburton, Brown & Root, Rockwater, Xtract Energy plc, Elko, Zenith Energy, Edison Mission Energy. Alan is among the five largest shareholders.

Greg Harding, CTO, has held positions in BG, Gaffney Cline, Union Texas, Kerr McGee, Challenge Energy & Setanta Energy. Greg is among the five largest shareholders.

Joe Darby, Chairman, has held several executive and non-executive positions in O&G companies in the UK, including Setanta Energy or Faroe Petroleum.

Risks

ORCA does not have any revenue, should the negotiation of the farm-out deal or the approval by the NSTA fail, the company may lose all key licences and be in a position to make an extremely dilutive placing to pursue the development of the licences applied in the 33rd licencing round. In a few words, the outcome of this HoA is a life or death situation for the company.

The Pilot field is appraised by 7 wells, and Sproule allowed ORCA to consider the oil volumes as reserves, not resources, to show the maturity of the concept, as “justified for development”. This considerably limits the geological risk.

Conclusions

The situation was getting very dark for ORCA before the announcement of this HoA. Now the company seems to be on path to secure the farm-out partner that will cover the initial development expenses. ORCA was saved by the bell.

The name of the potential partner is a mystery, but we speculate with being a major company looking for a low-emission new development where it can benefit from the EPL allowances. Any company must have a strong financial capacity to invest US$200-300 million for the phase 1 of the development in the next 2 years, which would include the refurbishment/adaption of a chartered FPSO for the specific conditions of the Pilot field. There are 2 other FPSOs already operating in the area: Serica’s Triton (which is producing light oil that is not compatible with Pilot’s) and Hibiscus’ Anasuria (which is already booked for the Teal West expansion). In our opinion these could be candidates:

Harbour Energy: it is paying high taxes and the EPL allowances will be well received, but it is in the process of leaving the UK. Unlikely.

BP: at this moment it is a ship without a captain. Impossible.

TotalEnergies: it is in the process of changing its position about new o&g developments and it has not been very active in the UK in the past years. Likely.

Shell: it just left Cambo and it is selling mature assets. However, Pilot’s low scope 1 and 2 emissions fit its strategy, like the Victory gas field. Likely.

Neo Energy: it produces oil in the UK using different FPSOs, it also operates sub-sea tie-ins. Very likely.

Ithaca Energy: it has just assumed 100% of Cambo. Unlikely

Spirit Energy, APA corporation, Serica & Enquest: due to their smaller size, this HoA would have been a material event and they would have had to report the deal through an RNS. Very unlikely.

Other smaller companies include Viaro/Rockrose or Hibiscus and their even lower financial capacity makes them extremely unlikely.

There is still a risk that the HoA doesn’t become an agreement, because the partner may demand better conditions (this is unlikely IMO). Also, the NSTA has still to approve both the transaction and the extension/grant of the licences, which adds some uncertainty to the situation, but we believe that the transaction is also of the interest of the NSTA, whose goal is to increase o&g production despite the public messages sent by some British politicians and environmental groups.

Hence, the transaction will provide ORCA with access to 14.7 MMbbl of 2P reserves (with an EV of little more than £1 per barrel), which would receive a premium over Brent due to the low sulphur content that makes it ideal for diesel production. Also, the use of the polymer flooding assures that the production will extend over a longer period of years compared to traditional developments, with a smoother production curve. In addition, a potential extension of Pilot with Elke and Narwhal will make the deal even more attractive.

Despite this farm-out deal, the total consideration would be US$3.2 million, and £1 million has to be used to repay the STASCO loan, so the net consideration would be £1.5 million, which may not be enough together with the last placing to cover the expense for the next 2 years (we think that Steve and his team will not stop here). In case a new opportunity arises in the new licences from the 33rd round, there could be future placings even if the farm-out agreement is signed but Pilot hasn’t reached first oil.

It is very important to consider that the stock is very illiquid out of days of high volatility like the past weeks. So, it is difficult to buy a position. That could explain some large swings in the share price.

Disclaimer: at the moment of writing this article, we don’t hold shares of Orcadian Energy. However, we may buy or sell shares at any time. This document only represents the opinion of its authors; its content cannot be considered investment advice and it has been prepared only for informative purposes.