Serica Energy: tradition meets modernity

An old-style UK company changing course with a solid balance sheet

I have recently started a position in Serica Energy (LON:SQZ) and I wanted to share here why I think it is bound to deliver positive surprises in 2024 and beyond. This post will not focus on the assets, which are not the main reason why I’ve bought some shares, but other aspects that are more appealing to me.

As a disclaimer, I don’t like the UK as an o&g jurisdiction, those who follow me on Twitter know it. I have mentioned Serica there a couple of times, and I think you could have seen that it is one of the few E&P companies in the UK that I have been somewhat positive about. As I see it, the politicians and part of the population are causing self-inflicted damage that will harm the future of the country and take the o&g sector down with them. However, everything has a fair price and, in this case, I can live with some Serica shares in my portfolio without being uncomfortable.

This post will try to go straight on point and these are the main 3 reasons why I think that Serica will outperform its peer in the UK:

quick overview of the company and the Tailwind deal

recent changes in the company

balance sheet

valuation exercise

future of the company

As we commented in the previous post, we are considering activating the paid subscriptions. We believe that these posts provide value, and many of you are likely reading not for the delightful prose and literary style, but because you expect to profit. The extensive research required for writing detailed posts consumes a significant amount of time, and I think it is fair that this is rewarded by those willing to support Zero GCoS. Eventually, this will be activated and I wanted to give a heads-up before it finally happens.

An overview of Serica

Serica Energy is an oil & gas producer in the UK. The company has built an diversified portfolio through several acquisitions in the last 10 years, including Erskine, Columbus, Bruce, Keith and Ruhm. The last relevant acquisition was Tailwind Energy, completed in March 2023, where it added a significant amount of production. In the last 12 months it has closed a minor purchase of a stake in the Greater Buchan Area licence.

The company is currently producing oil and gas in Northern and Central sectors of the UK Continental Shelf. All assets are offshore and 80% of them are operated by Serica:

The production comes from 11 different fields, which ensure some diversification. In reality, such diversification is lower than it could look like, as there are certain central processing and transportation infrastructure that are shared among different fields, for example, the Forties pipeline serves BKR, Columbus and Erskine.

It is important to highlight that Serica has decided to avoid exploration activities as they are inherently risky and the fiscal framework isn’t particularly supportive. The last attempt was North Eigg in 2023, where the company failed to encounter economic amounts of oil, and the licence was relinquished.

Assets overview

By the end of 2023, the company had 2P reserves of 140.3 MMboe, split as follows:

oil: 69.6 MMbbl

natural gas: 410 Bcf (70.7MMboe)

With an average production of c.14MMboe the last years, Serica has a reserve life index of 10 years, which could be extended in the case that the NSTA approves some of the FDP submitted.

Serica achieve an average production of 40,121 boepd in 2023. Below there is a high-level breakdown of assets and their production in 2023:

Bruce (98%), Keith (100%) & Rhum (50%) - production: 18,977 boepd

Triton Area (Bittern 64.63%, Evelyn 100%, Gannet E 100%, Guillemot West & North West 10%, Belinda 100%) - production: 14,150 boe/d. Belinda’s FDI was taken and the NSTA has recently approved its development.

Columbus (75%) - production: 2,180 boe/d

Orlando (100%) - production: 3,514 boe/d

Erskine (18%) - production: 1,325 boe/d

Greater Buchan Area (30%) - redevelopment. FDP submitted to NSTA.

Mansell (100% ) - redevelopment

Skerryvore (20%) - exploration. A commitment well before October 2025.

However, the numbers above don’t show the full production capacity of Serica. The company suffered several production problems last year, affecting the FY2023 production:

Production in the second half of the year was lower than the first half due mainly, as previously reported, to the planned summer shutdowns for both the Bruce and Triton hubs overrunning to rectify safety related issues. There were also a number of facilities issues on Bruce and Triton which caused short-term interruptions to production late in the year and carried over into early January. These are now largely resolved.

Notwithstanding these issues, production in the fourth quarter of 2023 averaged 45,748 boe/d.

Besides achieving substantial production, the portfolio includes several redevelopment or low-risk development opportunities in Kyle (Triton Area), Buchan Horst (Greater Buchan Area), Belinda or Mansel. For example, the company will complete in 2024 a light-well intervention campaign in the Keith field to replace an ESP. These low-risk opportunities would use existing infrastructure like platforms, FPSOs or pipelines, which will reduce the development costs and future decommissioning liabilities.

A flawed policy ruining a sector

The situation at GBA is particularly interesting and it provides a very good understanding of the current situation for the oil and gas sector in the UK as a result of the Energy Profit Levy (EPL).

Serica completed the acquisition of the 30% interest from Jersey Oil & Gas in February 2024. The idea behind the deal was to participate in a low-risk redevelopment with additional upside in other undeveloped discoveries (J2 and Verbier). Buchan Horst’s FDP was submitted to the NSTA with ongoing pre-FEED studies and negotiations to secure the Western Isles FPSO and connect the field to an adjacent wind farm for reducing the GHG emission intensity. The redevelopment was progressing well, with a first survey completed and a second survey being planned for this month. The FID is now planned for 2025, with first oil in Q1 2027 (originally Q4 2026). Nevertheless, it would still have to deal with the EPL until 2029.

The 80% investment allowance of the EPL plays in favour of this development. It will allow partners to reduce the ‘temporary levy’ of 35%. However, the announcement of the elections in the UK - the labourists seem to be the only condenders - and the aggressive stance of the labourists with regards to continuing oil and gas production in the North Sea have casted some doubts over these plans:

project sanction is naturally linked to securing fiscal clarity from the next government and ensuring that the project remains financially attractive

The opinion of this tourist is that they have not yet pulled the plug, but may do so later if the new government passes laws that harm the project's profitability. The partners will be watching in case the conditions of the EPL are worsened or an even more terrible policy is announced by the new government.

The labourists have proposed an increase of the temporary levy to 38%, the most critical aspect is the potential cancellation of the allowance. They estimated in January 2024 that this policy will reduce CAPEX across the oil and gas sector by 1/8 in 2027, 1/8 in 2028, and 1/4 in 2029. In any case, the announcement made by the Buchan partners is the perfect example of what negative and inconsistent policy causes in a highly profitable sector, one that pays billions in taxes and directly and indirectly employs more than 120,000 people in high-paying jobs.

The future of the oil and gas sector in the UK looks grim. The new government could re-affirm the attacks on the sector with a short-sighted policy that doesn’t care about the actual well-being of the citizens. It is difficult to understand the strong support received by the belief (I use that work because it is not supported by facts) that oil and gas is only a problem forgetting that it is also responsible for the progress that many occidental, modern economies have enjoyed in the last century. Dark times …

The ‘new’ Serica

The company had had a very good 2022 thanks to the sharp rise of the Energy prices. However, the oil hedges over the oil and, particularly, natural gas reduced the profit. Then the EPL put another nail on the coffin for Serica’s 2022. That same year it entered into a stupid corporate fight with Kistos’ management, involving respective acquisition offers that aimed to harm each other rather than provide value for shareholders. The initial offer made by Kistos included: payment of £2.46 per share plus 0.29 shares of Kistos. At that moment, the price was equivalent to £3.82 per share, which doesn’t look bad compared to today’s price, almost 50% of that.

After the deal/merger with Kistos was cancelled, Serica announced in December 2022 an agreement with Mercuria to acquire Tailwind Energy. The terms of the deal were:

111 million shares to Tailwind shareholders (equivalent to ~£308.7 million),

£58.7 million in shares,

£215 million in assumed debt at completion.

Although, the price of £585 million seemed high considering the 42 MMboe in 2P reserves. Anyway, Tailwind’s production of 40,000+ boepd was higher than Serica’s 26,200 boepd in 2022. Another positive aspect of the deal were Tailwind’s tax losses of $1,366 million of UK Ring Fence Corporation Tax losses and $1,202 million of Supplementary Charge losses, at a time that Serica had already utilised all its tax losses. All in all, the deal was positive for Serica’s needs: more production, better oil-gas ratio and addition of tax-losses.

From the perspective of the 2 businesses, the transaction made sense; it combined Serica’s gas-weighted portfolio with Tailwind’s oil-weighted portfolio, creating a balanced company. Let’s look at the production of Serica in the last years, and let’s focus on the oil-gas ratio:

In my opinion, Serica’s production profile now is better than it was before. I’d rather have a balanced production than 90% of oil or gas. The gas in Europe is very expensive compared to the US, but on the other hand, the oil market is more stable, and that gives better oversight over the future price of the production. A balanced production in the UK is still good, even after the drop from the record levels in 2022, the production of gas is very profitable. At today’s price, the TTF is still trading at more than double its historic average (€33MWh vs. €15/MWh, or $60/boe vs. $27/boe). However, the real problem for Serica as of today isn’t the oil or gas price but the high tax levels.

The main criticism to the deal is that the company had accumulated £432.5 million in cash by the end of 2022, so it had more than enough resources to complete the acquisition without increasing the shares outstanding by 40%. The conditions of the deal showed that the management was desperate to close a deal. The huge cash position was a time bomb, it could have been used by another company to acquire Serica and use its own cash reserves to pay for it. Something that was part of Kistos’ offer.

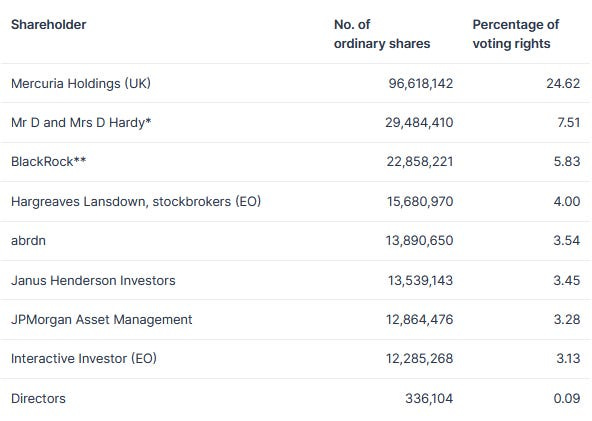

Serica completed the transaction in March 2023 and it was evident that it looked more like a reverse take over than a proper acquisition. As a result, Mercuria has become the largest shareholder of Serica with more than 25% (it has been slightly reduced since then).

A partnership with Mercuria is always a good thing, but the previous leadership let Mercuria dictate the terms in its favour. In fact, management and directors were also signing their death sentence. One of the main changes after the deal was completed was the replacement of all top management positions and some of the directors. The timing of the changes was a follows:

March 2023: Mercuria nominates 2 directors (Guillaume Vermersch and Robert Lawson) and appoints 3 members of the management team (Steve Edwards, Dave Freeman and Tom Ujejski) in temporary roles.

May 2023: Serica’s Chairman (Antony Craven Walker) steps down, leaving the position for David Latin.

November 2023: the CFO, Andy Bell, resigns and is replaced by Martin Copeland.

December 2023: the 3 members of the management team complete their temporary roles.

February 2024: the CEO, Mitch Flegg, announces his resignation.

April 2024: Mitch Flegg is replaced by David Latin as interim CEO and the company announces a buyback program (marking the beginning of a new era?).

May 2024: the new CEO, Chris Cox, is announced, his tenure will begin on 1 July 2024.

Among the key positions, only the Chairman has been part of Serica prior to the Tailwind acquisition. The new CEO and CFO combine experience in the North Sea with a long list of M&A transactions in the North Sea. These changes mark the transformation of Serica from the old mindset to a new approach to conducting businesses in the oil and gas sector.

The new CEO

The soon-to-be new CEO, Chris Cox, has experience in the UK o&g sector as well as in international operations. One of these key roles was his tenure in Centrica, from where he was appointed as CEO of the subsidiary Spirit Energy. He was responsible for managing Spirit’s assets in the UK, The Netherlands, Denmark and Norway. Hence, he has experience in working at companies with a diversified portfolio, more on this later.

Additionally, Chris’ appointment to the board of Capricorn Energy in February 2023 was noteworthy. He joined it after a radical change of strategy, when the former leadership was ousted by disgruntled shareholders that demanded improved value creation for shareholders. Part of this new strategy was to minimise exploration effort and chase organic and inorganic growth opportunities with extraordinary distributions to shareholders being a key element. He acted as interim CEO while the company searched for a permanent CEO, and left the company in June 2023 (he may have intended to stay in the role). Hence, he has experience in situations where implementing radical changes is the core strategy.

The new CFO

The role of Martin Copeland is also very relevant for the ‘new’ Serica. Martin has been working on many large acquisitions, sales and mergers during his tenures at Kirk Lovegrove & Company, RBC Capital Markets or Evercore. So, he is more than capable of managing large transactions in the oil and gas sector. In my opinion, his nomination as CFO confirms Serica’s intention to secure a pipeline of M&A opportunities and close at least one deal in the short-term.

Martin participated in the reverse takeover of Premier Oil by Chrysaor that created Harbour Energy (he may have Linda Cook’s phone number in his agenda) and the sale of JX Nippon’s former British assets to Neo Energy.

Some of the deals where he participated are very interesting, as it is described in more detail later …

A solid company

The company released the annual results on the 24th of April and they were not brilliant, but they weren’t bad:

revenue: £632 million

net income: £103 million

operating cash flow: £65.6 million1

FCF: (£18.9) million2

I was expecting a worse year, as 2023 was the first complete year of the EPL. The EPL entered into force on 26 May 2022, so the 2022 and 2023 financial results cannot be compared without introducing some adjustments.

The financial position of the company by the end of 2023 was very healthy:

Cash: £263.5 million

Debt: £213 million

Tax assets: £84 million (vs. tax liabilities of £153 million in 2022)

ARO liabilities: £116.5 million

Net cash position: £75.9 million

One of the aspects that I liked the most is the low ARO liabilities compared to the assets it owns, which are not young. This is something that very few companies in the UK have, as most of them have high liabilities for the next few years. Most E&P companies operating in the UK have high liabilities that put the future of the companies in jeopardy. The EPL doesn’t include allowances for decommissioning, so the tax rates aren’t lowered

Large funding available

Another key aspect is the access to funding, which has been improved since Mercuria joined the list of shareholders. In December 2023, Serica signed a new RBL facility, increasing the available liquidity to US$1,050 million. The maturity of this new facility is by the end of 2029, which gives the company enough room to make use of the funds. These are the main details:

The main covenant (net debt to EBITDAX of 3.5x times) shows that the RBL gives plenty of room to use it to acquire other assets or companies, not only for investing into the existing business: “Significantly increased liquidity to support future acquisitions and investment”. Hence, I believe that this RBL marks Serica’s active pursuit of at least one large acquisition. If that’s the case, it could change the course of the company and divert it from the UK, or, in the worst case, diversify it.

Shareholder return policy

The company has been traditionally seen as a dividend stock by many UK investors, and most discussions were centred on maintaining or increasing the dividend using the large cash position it had. That mindset is very common in the UK, but the company demonstrated one more time that is open to change and announced its first buyback program with the publication of the 2023 results:

London, 24 April 2024 - Serica Energy plc (the "Company") (AIM: SQZ), a British independent upstream oil and gas company with operations centred on the UK North Sea, today announces the initiation of a share buyback programme to purchase ordinary shares of US$0.10 each in the Company for up to a maximum aggregate consideration of £15 million from the date of this announcement (the "Buyback Programme").

The program was announced the same day that Mitch Flegg stepped down from the CEO position, which is a curious coincidence …

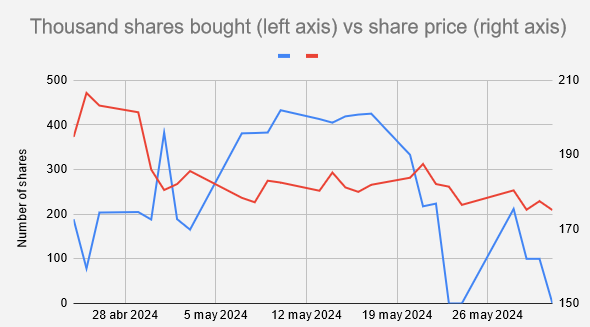

The company has made a strange use of this buyback program with an initial steady level of 200,000 shares that grew to exceptionally high levels of 432,000 shares. The purchases have been extremely inconsistent in the last 2 weeks, with many days without any purchases at all. The program could have been used in just a few weeks at the initial pace. The effect of the buybacks has been reduced by the use of 5.45 million to satisfy the exercise of employee share options and share incentives, with the remaining 1.15 million shares held in treasure. Those shares would have been issued without the program, so the program has helped in reducing the outstanding.

The company may be trying to extend the duration of the program, but it looks like there is some kind of discretionary use of the purchases, as the volume has been so inconsistent. This week was a good opportunity to use the program to reduce the average price paid, instead, Serica has decided to limit the purchases to 2 days (they may have bought some on Friday, but we won’t know until Monday) with a low volume, just 100,000 shares each.

To be honest, this is difficult to explain, and it doesn’t speak particularly well of the ‘new’ Serica. One would think that they would have deployed the program in either a steady way (150,000-200,000 share per days) or opportunistically (buying more the days the share price drops). The situation right now is something in the no man’s land that isn’t satisfactory to anyone (at least, it isn’t to me). Hopefully, we will learn in the future how the program has been managed and the reason behind its irregular deployment. Could they extend the duration of the buyback program until the new CEO arrives? That would be stupid, but you know … “Never attribute to malice that which can be adequately explained by stupidity“

So far, the program has already acquired 6.6 million shares, spending £12.7 million out of the £15 million. There is just £2.7 million left in the current buyback program, which could last 1 week or 1 quarter, depending on the future purchase rate. After seeing how the current program has been managed, I don’t expect the company to renew it, but it could be a surprise for the better …

Share price

I said before that the company is solid, but its share price isn’t. The evolution in the last year has been terrible, the UK gas price has continued its downward trajectory and the winter weather was quite mild. The negative return has been 33% with 23p paid in dividends, which lowers the total return to 23%.

This week, the share price broke the 175-180 level that was acting as the floor for the share price in the last year. It could go below 160 and only God knows where the share price will go from there.

A negative aspect that is worth mentioning is the listing. Serica is still listed in the AIM, which is the space for microcap companies and not for a company with a Mcap of £635MM. Unfortunately, many of you in the US or Canada use brokers without access to this market. Sincerely, I don’t understand why Mercuria hasn’t changed this, unless it doesn’t care about today’s share price or easing the access to the company for Institutional Investors. Mercuria may have a forward looking vision, expecting that Serica’s fair value will materialise through the sale of the whole company when the right time comes. Anyhow, a change of the listing would be desirable.

The future of Serica

What turned my neck towards Serica was this piece of news: Aker BP and Serica Energy interested in Sval Energi The source seems to be Bloomberg, but there isn’t another source confirming this. The sales process had been announced by the start of the year, but there wasn’t any information about how the sale process was going. Additionally, there is another mid-player in the North Sea that has been put on sale this year, NEO Energy. WoodMackenzie made a short video about both companies, which I recommend. One very interesting aspect is that both companies are owned by HitecVision, and the combined production is estimated at more than 150 kboe/d.

From the 2 transactions, Sval Energi seems to better fit what Serica has been commenting on in the last year, with a focus on internationalisation, but the option of chasing NEO Energy doesn’t seem totally discarded by the last company update on the outlook:

In this video, David Latin, the interim CEO and Chairman, insisted that “we’re looking particularly in Norway, but we won’t forget about the UK either”. Thus, my base case is that Serica is more interested in Sval Energi than in NEO Energy.

Who is selling Sval Enegi? A private company called HitecVision. This company founded UK-focused NEO Energy which completed a $1.66 billion deal with JX Nippon in 2021 for the acquisition of its British assets. Do you know who advised the process? Martin Copeland! Current Serica’s CFO played an active role in the sale process by advising the “other side” (the seller JX Nippon). So, Martin has experience dealing with HitecVision.

But this is not it, Sval Energi was created through acquisitions, and one of the deals was the purchase of Spirit Energy’s assets in Norway in 2021. Chris Cox was directly involved in the management of these Norwegian assets during his tenure as CEO of Spirit Energy. So, if the acquisition of Sval Energi completes, Chris would again lead a company with a portfolio covering the UK and Norway that includes assets he knows perfectly.

Hence, we may wake up one day to the announcement that Serica acquires Sval Energi or NEO Energy. We shouldn’t fool ourselves thinking that there is a done deal, it could go the other way and be acquired by Aker BP. Although, I’m sure of one thing, Serica will make a huge acquisition soon. Is 2024 feasible? I don’t know, but I think it is very likely that something will be closed during 2024.

Remember that Serica has a RBL facility with up to $1,050 million of liquidity, and together with its current cash position, it allows it to chase large acquisitions. In the case that a transaction would require even more funds, I don’t think it will be a problem for Serica to extend the liquidity by issuing a bond linked to the acquisition.

Meanwhile, the company has secured one of the best deals: buying its own shares (in a limited way though). Thus, I interpret that the decision to acquire shares is to break with the past. One of the most controversial decisions by Mitch Flegg was to accumulate insane levels of cash in the balance sheet. Now, the company prefers to put the cash to work for its shareholders instead of just sitting on its bank account.

Another confirmation that the company is looking elsewhere from the UK is the result of the 33rd licensing round, where Serica only applied for the Kyle field (licence P2616). Kyle is an infrastructure-led development located 20km southeast of the Triton FPSO. In case the company gets the approval for its FDP, the development cost will be modest with the field tied to the existing FPSO. Additionally, the company was awarded 1 licence in the 32nd licensing round that it relinquished after completing some subsurface evaluation.

The strategy that the new management is applying is crystal clear to me, they will extract all value left in the British assets they already own, but the focus is on expanding outside the UK. This is something they share with Harbour Energy, another company where I’m invested at the moment.

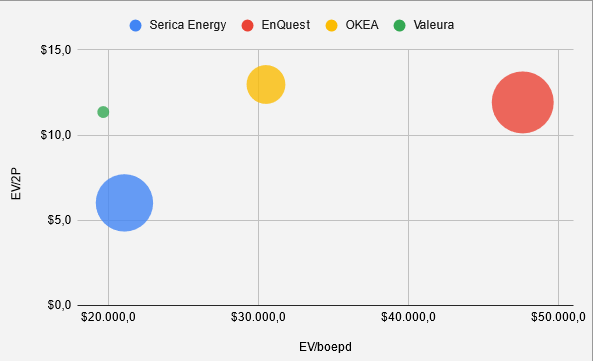

Valuation

In order to make a fair valuation, we will compare Serica to other peers of a similar size. The main problem is finding companies that are mainly operating in the UK but are also working to expand elsewhere. Two other companies of a similar size are the British EnQuest (43,812 boepd) and the Norwegian OKEA (35,385 boepd). Both companies operate mature assets in the North Sea (EnQuest owns some international assets, but they are not representative).

In order to provide some context to this valuation effort, I think Valeura Energy could be useful as a benchmark of what a low reserve-based valuation looks like. Valeura’s low EV compared to the current production is justified by its limited reserves life index, which is being penalised by the market.

The valuation exercise will consist of comparing these companies according to production, cash flows and reserves. However, Serica’s 2023 accounts don’t show any FCF generation due to the high tax rate and capital program. Moreover, its 2023 accounts include Tailwind’s assets from the 23rd of March, which leaves almost 1 quarter out of the picture. That means that I would have to create a scenario with the pro-forma numbers, where the company paid less taxes (due to the tax losses) and slightly higher CAPEX, which is not a realistic exercise. Instead, we can use a metric that I personally do not like, but it could reflect in some way the cash flow generation potential of the company, adjusted operating cash flow (OCFx), excluding financial costs/income and acquisition-related one-off costs.

The comparison of the 4 companies is the following (using the same methodology to adjust the working capital and leases, and calculating net debt using working capital, inventory, debt, deferred tax and tax liability/payable):

First, let’s compare their EV using the production and 2P reserves. The graph below shows the result, with the size of each bubble displaying the RLI, the smaller, the lower:

Do you remember that Serica has some operational issue during 2023? If one adjusted the production to the level achieved in Q4 2023, even with some ongoing operational issues, Serica would be the cheapest in both categories.

The comparison above shows the deep discount of Serica versus these peers, if we only consider reserves without any kind of distinction between natural gas and oil reserves. By looking at the oil weight of the 2P reserves, Serica doesn’t look good in the picture, and this explains part of the discount:

Serica: 47,9%

EnQuest: 75,8%

OKEA: 76,7%

Valeura: 100,0%

The resulting valuation below is just the average of the 3 other metrics (I removed Valeura because it is even cheaper than Serica, and that’s the reason why it keeps being one of my top positions):

As it can see above, Serica has a much stronger balance sheet and much lower ARO liabilities compared to these peers, but the valuation doesn’t show it. The downturn is the low weight of the oil reserves, which is impacting the valuation at the moment. Despite being the one with the least liabilities including debt and ARO liabilities, $37 million, the market isn’t reflecting it. As we used EnQuest in this comparison, the effects of the EPL and jurisdiction aren’t the reason why it could be so ignored by the market.

Conclusion

In summary, Serica Energy is a British company that is doing the right thing:

changed the management and board,

reduced the investment in the UK in response to the EPL,

prioritised low-risk opportunities such as Belinda and Buchan to use the allowances of the EPL,

increased the return to shareholders with dividends+buybacks, and

started a M&A process to expand beyond the UK.

The outcome of this transformational process is uncertain, but the return to shareholders seems to be guaranteed, at least while they don’t find a sizable M&A target. This year, the company should beat the 2023 production by some margin. The low-risk, organic growth prospects provide a floor to the production in the next few years, which gives certain reassurance over the future of the business in the next 4-5 years. The expectation of inorganic growth is supported on a strong balance sheet and the financial backing of Mercuria. I don’t have any doubt that Mercuria will step in to provide the necessary funds, if necessary to complete an operation as large as Sval Energi or NEO Energy and the existing $1,050 million liquidity wasn’t enough.

In my opinion, the part I like the most is that the market isn’t pricing in any potential new deal, but the new team seems to be fitted for that task. I think Serica’s share price could provide an interesting return in the next 12 months just by continuing drilling its low-risk redevelopment opportunities and distributing dividends and buying-back shares. In the case that it manages to close a transformative acquisition like Sval’s, the share price could easily double. This time the company has already secured the financial resources for a large acquisition, and HitecVision doesn’t seem interested on continue being a shareholder, so I don’t expect them to dilute current shareholders as they did with Tailwind.

The new CEO is joining on 1 July, why would the company announce a large acquisition with an interim CEO? I can image that Chris Cox would like to arrive to the job with a positive announcement, sending a strong message to the market that Serica should be ignored no more. We may know this summer if these speculations over a large deal are totally BS, because I don’t think that the outcomes of Sval’s and NEO’s sales processes are very far in time. In any case, I do expect some deal to be announced in 2024 or early 2025.

The major uncertainty at the moment are the result of the British election and the measures by the Labour winning party with regards to the oil and gas industry. If the labourists win the general elections, I don’t think they will wind down their plans for removing the allowances and increasing the tax rate of the EPL, but they could give some concession, like not extending its duration. It’s a complex situation that, at the same time, incentivizes Serica to look elsewhere beyond the UK.

Some negative aspects of the company are also internal. The company hasn’t been unable to implement the buyback program in a convincing way, and that’s something they should fix asap. With the share price severely undervalued, it is a good moment to be aggressive with the purchase of shares, particularly when your cash position is half your market capitalisation. The £15 million of the last program is a joke compared to what the company should be spending, but they may be preserving cash for something …

I like the convexity of the idea, little downside at current levels of 162p (8.6% dividend yield, so far) with a high upside. My portfolio has significantly changed during 2024, with the sale of Vaalco and entry of Sintana Energy, Serica Energy and Seplat (you should look at Seplat’s deal with ExxonMobil). I like that all these ideas don’t depend of the oil price as much as my beloved Valeura, so it gives me exposure but with different catalysts. I am not very bullish on the oil price for the remaining of the year, but I do think that these companies are bount to provide significant returns.

Disclaimer: the authors own shares of some of the companies mentioned in the text, which they may sell at any moment. This post has been prepared only for informative purposes. This is not investment advice.

own calculation

own calculation

North sea is toast and with it SQZ. Here's what the incoming Labour govt. will do:

Labour will close the loopholes in the windfall tax on oil and gas companies. Companies have benefitted from enormous profits not because of their ingenuity or investment, but because of an energy shock which raised prices for British families. Labour will therefore extend the sunset clause in the Energy Profits Levy until the end of the next parliament. We will also increase the rate of the levy by three percentage points, as well as removing the unjustifiably generous investment allowances. Labour will also retain the Energy Security Investment Mechanism.

Thanks for the considerable time and effort you have extolled in this piece, so others, like me, don't have to.

And having written similar pieces, I know the effort/time involved. So thank you.

(And yes readers here should definitely look at SEPL.).