Update on Zero GCoS companies

Summary of recent events for the companies we've previously covered

Yesterday, we activated paid subscriptions as some subscribers requested them to show their support to us. You may think that this is the end of Zero GCoS, but it isn’t. We will continue publishing at least 1 write-up every month for all subscribers, but paying users will enjoy access to the complete archive (after 3 months, next write-ups won’t be available to free subscribers). We have also activated a time-limited founding subscription at $99, which will maintain a fixed price for the future, with no price increases ever. The services offered to paid subscribers will be extended in the future, along with potential adjustments to the price.

As there have been many new subscribers in the last week, we wanted to provide an update regarding the o&g companies previously mentioned in Zero GCoS. We will do a similar post with their Q4 results, once they are published.

In case you haven’t done it yet, we encourage you to visit the write-ups about the companies below before reading each update (click on the title of each company). From time to time, we will publish specific posts coincidental with material events for one of the companies covered, as we did with Longboat Energy or BW Energy in the past.

There isn’t much to comment about, there hasn’t been any operational update since the publication of the article. The company hasn't reported any progress on the farm-out in Vietnam, which is crucial for the company's future, given that its other assets are not particularly exciting.

The company confirmed an interim dividend of 0.33p (1.5% yield) and allocated an additional $3 million to the buyback program, bringing the total to $9 million, which will acquire approximately 7.5% of shares.

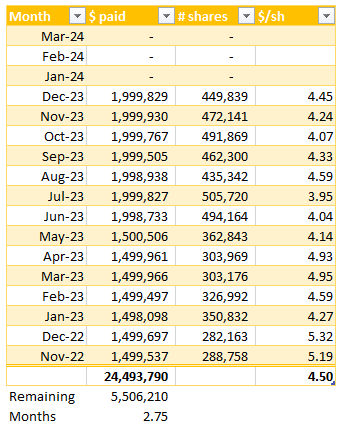

Bradley Radoff has continued purchasing shares, and he now holds more than 59 million shares (14.1%). The CEO and CFO have continued their monthly share acquisitions, aiming to adhere to the ownership policy.

So, there have been few changes to the company, whether for better or worse.We still anticipate progress in the farm-out process or confirmation of an infill drilling campaign in the existing TGT and CNC fields. The settlement of the Egyptian receivables or a potential sale of those assets would also be positive news for us. We will keep monitoring Pharos Energy, but it is still a speculative investment, because Bradley Radoff’s intentions aren’t totally clear yet.

After the failure in Velocette, the company confirmed in its Q3 results that the $30 million contingent payment is gone with an additional $4 million contingent on the closure of the acquisition of minor interests in Statfjord Øst and Sygna, which is expected this month.

In Q4 2023, its JV with JAPEX has farmed down its stake in 2 exploration licences (Lotus and Jasmine/Sjøkreps) in Norway for a carry in the next stages of exploration. This farm-out will reduce the capex required next year (Lotus well planned for Q3 2024) and it could use the available funds in other licences.

While in Malaysia, it continued with the plans to increase its stake in offshore Block 2A after completing the acquisition of Topaz and the addition of its team.

Given that the JV hasn’t employed the $100 million acquisition financing facility, Longboat’s JV could acquire more producing assets at any moment.

In summary, there has been little progress from Longboat in the last months, nevertheless, the strategy remains the same, yet the risk is high as in any exploration bet.

We liked the Q2 2023 report as production was higher and both capex and opex came lower. We capitalized on the share drop following the coup d’état in Gabon and acquired some shares. The operational efficiency continued in Q3 2023 with production in the high range of the guidance. Although, the bottom line was negatively impacted by a non-cash tax item that will revert in Q4.

The company also has kept buying back shares ($2M/month) and paid a quarterly dividend of ¢6.25/sh. The buyback program is scheduled to run until March 2024, and we hope the company will confirm in the year-end update whether it intends to renew it or not.

We expect no surprises in the Q4 results and would like Vaalco to confirm the positive operational momentum.

With more than $100 million in cash, a progressive recovery of the Egyptian receivables, and an undrawn RBL of $50 million (which can be increased), it seems like the right time for Vaalco to make a move and pursue some inorganic growth.

It has announced today a dividend of 0.25p/sh (annualized yield of 10% at current share price).

The natural gas price in Canada has recovered in January and the AECO price is now in the C$2-2.25/GJ range. This comes after a challenging December when prices stayed below C$2/GJ for most of the month. The WCS-WTI differential is again above US$20/bbl, which reduces the netback from its oil production (22%).

In Q3 2023, i3's gas production was 44% and its liquid production was reduced due to some apportionment issues, and resolving these problems might take several months. Undoubtedly, the low natural gas and oil prices in Canada are impacting the company's profitability. We'll soon know the extent of the impact on the Q4 results.

The company planned the drilling and completion of 3 wells in Q4 2023 for a cost of US$6 million. These wells will begin producing after year-end. In the UK, the company announced a revision of the plans for Serenity now that the licence of the adjacent Tain field has been relinquished by its former licencees and it has become available.

In light of the situation, it seems that the strategy hasn't changed, Serenity is still on the table and the dividend remains a priority, despite its extensive undeveloped acreage in Canada, some of which is oil-rich. We believe the company isn’t appealing until it undergoes significant changes to its current strategy. We will stop following the company until the ‘shake-up’ that we were expecting materializes.

The production figures in Q3 came below the initial expectations. The ongoing ramp-up process is slower than initially expected. We had anticipated that adding another workover rig and a drilling rig would accelerate this process during H2 2023. The company was also impacted by lower than expected liftings that required it to curtail some production. The IMO 2020 spec has been delayed from early Q3 2023 to Q1 2024, which has caused some revenue losses due to higher pricing.

In early December, the company needed to raise $25 million to strengthen the balance sheet, part of which was necessary to satisfy a contingent payment to Petrobras of $35 million. The announcement of the placing was preceded by a series of positive news published in the week regarding the increase of production, which doesn’t speak well of the management, as they could have tried to artificially increase the share price. I would be quite mad if I had bought after reading a release titled “production recovery running well ahead of guidance”.

Yesterday, the company announced the issuance of an unsecured bond, the amount is still not public. This has been caused by lower production and pricing than previously forecasted during the IPO and completion of the acquisition of Norte Capixaba.

As a result, we have lost faith in the management of the company, as they have been unable to deliver. The substantial financial leverage has proven unmanageable without external funds. The share price should recover at some point, but the company is less attractive to us than it was. We will only cover it again if we see a significant change.

This young company began trading the day after our write-up and the price quickly rose above our initial price estimations to C$1.25, since then, the price has fallen to around C$0.8.

During H2 2023, Logan drilled its first Montney well in North Simonette (oil play), where initial production reached 732 boepd, comprising 67% oil and 69% liquids. It also drilled the maiden well in South Simonette (gas play) with initial production of 1,352 boepd with 27% liquids, climbing to 1,598 boepd and 36% liquids by October. The results were beyond expectations, particularly at South Simonette, where the company proceeded with drilling a three well pad that will be onstream in August 2024.

Q3 production was almost 5,400 boepd with 24% liquids, and the guidance for H2 2023 was raised to 6,000 boepd (+20% over previous guidance). Logan has added more acreage to its Simonette asset, growing it to 588 locations with 582 still unbooked.

The capex budget for 2024 stands at C$120 million, allocating 53% for drilling new wells and 23% for infrastructure. This investment is projected to elevate year-end 2024 production to over 10,000 boepd, averaging 8,700 boepd throughout the year.

The company’s production is mostly natural gas, and this has been reflected in the share price. Considering the AECO prices below C$2/GJ during Q4 2023 and the pessimistic forecast for 2024, the good drilling results might not be accompanied by a healthy generation of cash flow from operations. Hence, we don’t discard a placing or financing during the year, in case AECO doesn’t recover to at or above C$3/GJ. While the natural gas stays at the current depressed levels, the share price will not recover its previous levels around C$1.

In Q3, Kolibri published the results of its Barnes 8-2H and Barnes 8-1H Caney wells. The former had an IP30 of 476 boepd, with 80% being oil. The latter had an IP30 of 390 boepd, with 81% being oil. The novelty was the Barnes 8-3H well, which is the first T-zone well that utilized the Company’s latest fracture stimulation technique. The well had an IP30 of 480 boepd, with 68% being oil, and showed lower decline than previous T-zone wells, which made it economic. These positive results incentivised the company to extend the capex program from 6-7 wells to 8 wells in the year.

The company decided to discard the Upper Caney formation in future wells and focus on the Lower Caney and T-zone. It believes that the Lower Caney still receives contributions from the Upper Caney, and such development is more profitable.

The Barnes 7-4H and 7-5H wells had an IP30 of 665 boepd, with 76% being oil, and 613 boepd, with 75% being oil, respectively. The next wells were the Emery 17-3H, 17-4H, and 17-5H, which encountered some operational issues during the stimulation, resulting in a longer clean-up process than usual. Also, some adjacent wells were affected, resulting in a temporary lower production. The company said that this will reduce the year-end production, but the affected wells will recover their production level previous to the shut-in at some point.

The company has already drilled one new well (Velin 12-9H) and spudded the next one from the same pad. Hence, Kolibri is ambitious as it has maintained a non-stop drilling, completion and stimulation program to progressively compound its production. After drilling the Barnes 8-3H well, the next reserves report will recognise reserves in the T-zone formation for the first time. With total proved + probable 2022 reserves at 54 MMboe, the 2023 figure can reach a ridiculous amount compared to its Enterprise Value of just $140 million.

The Q2 production was 2,415 boepd (+25% YoY), and Q3 production grew to 2,737 boepd (+61% YoY) despite some gathering issues. It is important to remember that during drilling, completion and stimulation, adjacent wells have to be shut-in to protect them, which slightly affects the production in times of high drilling activity.

In November, Kolibri completed a dual-listing of its shares in the Nasdaq, ticker KGEI.

Kolibri should recover from this hiccup once the production rate from all wells is back to previous levels and the latest Emery wells come onstream. The company has had a very good operational history so far, and now it has unlocked the value in the T-zone. It is on a sweet spot, as the increase in production will begin generating more and more cash flows, and the proven stimulation technique has increased the value of its acreage. Hence, it could start distributions to shareholders or sell the assets to one of the major operating in the same area, such as ExxonMobil to which it sold the Woodford shale gas asset in the past.

In November, it completed a Bought Deal Financing of C$80 Million for the Two Rivers East project - including completion of the 5-19 pad and related infrastructure - and for general corporate purposes. It issued 33 million warrants with an exercise price of C$1.05 that expire after 12 months.

Vermilion participated in this financing and added 21 million shares to its holding. Now it owns 88.7 million shares, representing 16.7% of all outstanding shares, plus 7 million warrants. Vermilion owns the acreage right next to Coelacanth’s in Money, its latest wells achieved an average of 1,150 boepd per well with 36% liquids in its first 180 days. Vermilion has planned drilling and completing 11 wells in that acreage during 2024 and it has already built infrastructure ahead of the increase of production. Hence, Vermilion’s experience can be shared with Coelacanth’s team (remember that they bought Leucrotta’s assets from the same team), and this can help them to minimize errors and maximize returns.

During Q3 2023 it drilled five wells at Two Rivers East (eight more to reach the permitted fourteen wells) and completed two wells at Two Rivers West. Four TRE wells will be completed in Q4.

Production in Q3 was 201 boepd, down from 287 boepd in Q2. However, the current production is not representative of the future of the company, aiming to produce 20,000 boe/d by 2026. This plan requires a significant amount of capex; 2024 and 2025 investments are estimated at C$123 million and C$91 million, respectively, with first positive cash flow expected in 2025.

The company stays focused on its strategy to develop its Montney acreage, and revenue and cash flow generation are not the priority at the moment. The low commodity prices may force the company to require external funding again.

The most relevant aspect is the exercise by the Gabonese government of its pre-emption right in the Assala Energy acquisition. As a result, the Gabonese NOC will acquire it from Carlyle Group. This possibility had been commented on by several African media, and the president of the country publicly announced it in its new year’s speech.

In Q4 2023, Maurel et Prom completed the acquisition of Wentworth Resources, which produces natural gas in Tanzania, however, it had to renounce to 20% in favor of the Tanzanian NOC, leaving its WI at 60%.

Maurel is still benefiting from the resumption of the oil exports from Venezuela, and the extension of the current 6-month window is essential.

Maurel’s stake in Seplat has significantly increased in value during 2023. The acquisition of ExxonMobil’s Nigerian onshore assets hasn’t been concluded yet, and it could push Maurel’s stock to previous all-time-high levels if it is closed.

Maurel is still interesting but less than it was before the cancellation of the purchase of Assala.

We have extensively covered the company in several posts, including one summarizing the most relevant points of the Q3 CC.

The company hasn’t yet resolved the problems with the Electrical Submersible Pumps (ESPs) installed in the Hibiscus-Ruche wells, and a permanent solution is expected in Q1 2024.

The mandatory offer (NOK 27/share) by BW Group hasn’t attracted the interest of many shareholders with just 145,775 shares bought. The offer ends on the 12th of January 2024, and the share price will resume its trading without the effect of this offer.

We anticipate an operational update within the next 1-2 weeks containing Q4 2023 data, where we hope to confirm progress in addressing the ESP issue.

Let us know in the comments what you think about these companies and share with us the name of other companies that you find interesting.

Disclaimer: this document only represents the opinion of its author; its content cannot be considered investment advice and it has been prepared only for informative purposes. Please, make your own due diligence and analysis.

Some inaccuracies on your i3e piece - 2 new wells are already on production before year end. Also only about 10% of i3e's production is heavy oil subject to the WCS differential - the balance of production is light oil. Also could you clarify what "shake up" you were expecting?

The tie-in of the 2 wells was planned in Q4, but then they have to clean-up before the actual production starts, that's why I thought initial production is expected more in early Q1 than late Q4. I think they even said they expect them to contribute in early 2024, but I may have made a mistake in my notes.

You are right about the MWS, but the trend compared to WTI is similar to the WCS, which is known by more people. The price differential is lower vs. WCS.

The shake-up was described in the write-up, basically it should focus on either CA or UK and prioritise development over paying a dividend. It was currently unsustainable and it had to be reduced in 2023, there could be more dividend cuts in 2024.